Floor Plan Lending Risks

The Top 5 Floor Planning Mistakes Dealers Make

Floor Plan Financing Peoples Bank

How Does Floor Plan Financing Work Nextgear Capital

Irs Proposes Guidance On Bonus Depreciation And Floor Plan Financing Boyer Ritter Llc

Top 5 Floor Planning Mistakes By Dealers Nextgear Capital

Dealer Floor Plan Finance Program

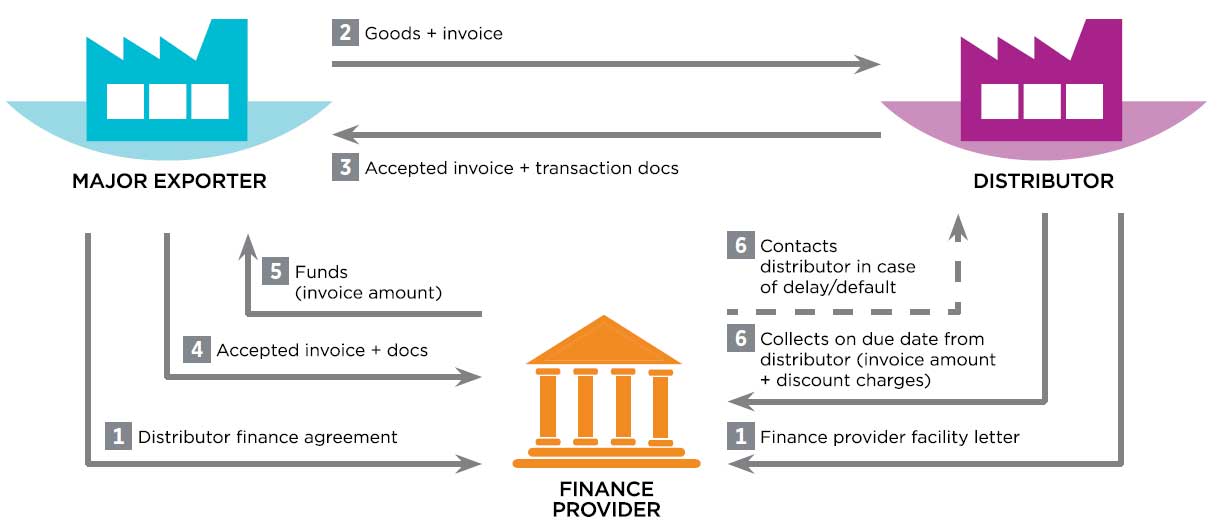

The dealer then receives payment hopefully including a profit and remits the balance to the lender who in turn releases the title to the car to the new purchaser.

Floor plan lending risks.

Distributor Finance Global Supply Chain Finance Forum

:max_bytes(150000):strip_icc()/GettyImages-99276138-164b389a35084e02b4b9a0305925365f.jpg)

Floor Planning Definition

Dealer Floor Plan Financing Fifth Third Bank

Basel Iii The Final Regulatory Standard Mckinsey

Bonus Depreciation Regulations Favor Taxpayers Grant Thornton

Dealer Financing Services Fifth Third Bank

House Plan 098 00297 Modern Farmhouse Plan 3 052 Square Feet 4 Bedrooms 3 5 Bathrooms House Plans Farmhouse House Plans Farmhouse Plans

فيلا 255 متر مباني و 286 ارض With Images Floor Plans Villa Areas

فيلا 449 متر مباني و 504 ارض Floor Plans Villa Aeg

Dealer Services Financing For Customers First Commonwealth Bank

Commercial Bank Floor Plan Design Pdf

Strategic Planning Template Ppt Unique Strategic Initiatives Powerpoint Template In 2020 Strategic Planning Template Strategic Planning Communication Plan Template

The Dangerous Unpredictable Risky Volatile World Of Commercial Shipping

Creditors Rights Financial Restructuring And Bankruptcy Mcglinchey Stafford Pllc

نتيجة بحث الصور عن Bank Layout Design Bank Interior Design Office Floor Plan Floor Plan Layout

Pin On Home Buying In Massachusetts With Maba Buyer S Agents

Traditional Style House Plan 75152 With 3 Bed 4 Bath 2 Car Garage House Plans One Story Family House Plans House Plans

Mezzanine Financing Basics And The Intercreditor Agreement Basic Commercial Real Estate Marketing Finance Binder Printables

3

Alliance Inspection Management Floorplan Audit

Auto Dealership Banking Solutions Suntrust Corporate Banking

Are You A Risky Borrower 4 Ways To Find Out Trulia S Blog Money Matters The Borrowers Home Buying How To Find Out

How Floor Plans For Car Dealers Make A Difference Nextgear Capital

Https Www Bostonfed Org Media Documents Events Stm First Gordon Pdf

Source : pinterest.com